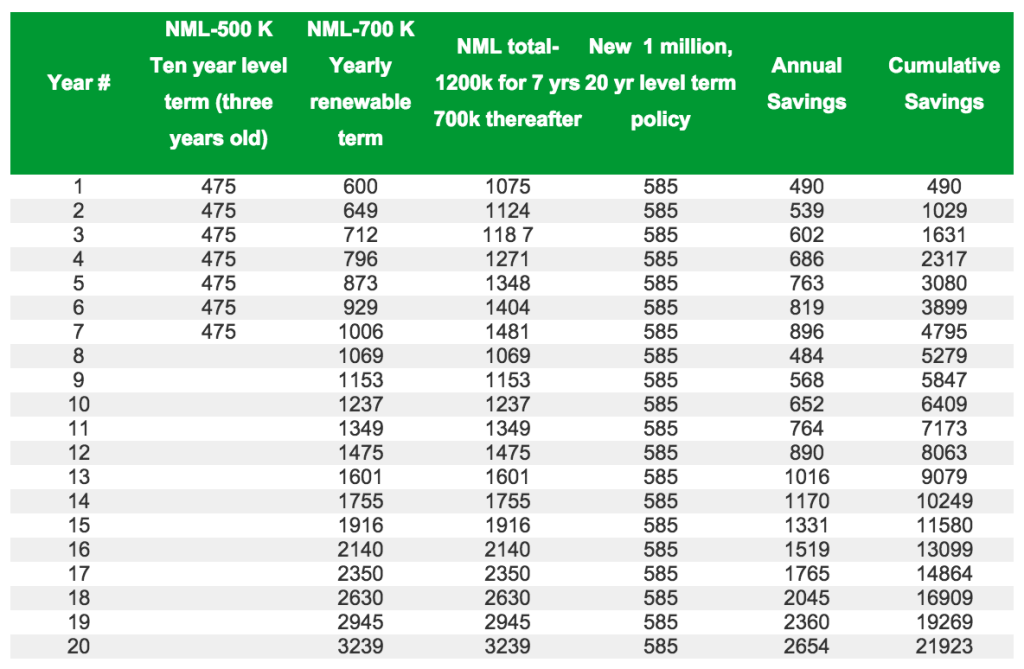

“I am an Insurance Salesman”: The Necessity of a Second Opinion Case Study # 9

I just finished a case that started as a call to the radio show, Money Wise. This listener’s agent encouraged him to replace a whole life cash with a new term policy and put the $45k cash value in an annuity. “Term is cheaper and the cash value will earn more”, sounded plausible. Mark Biller of Sound Mind Investing was the guest and recommended he call me.

First I evaluated the whole life policy to see if it needed replacing and then assessed his overall need for life insurance. The cash value was earning 3.87%, much higher than money in the bank, but lower than long-term equity investments. This wasn’t bad, but it was an inordinate amount of his net worth tied up in a relatively low long-term return.

He was no longer married, and had a 22 year old independent working son and 19 year old student daughter. He already had two good life policies: the 150k whole life and a 200k term policy costing only 342/yr with level premiums for another nine years, more than long enough to see his daughter to independence. The agent recommended a new $400k 20 year term policy costing 1492/year. He didn’t need insurance for 20 more years and he didn’t need that payment.

…there comes a time when emphasis needs to shift from the what-if-I-die scenario to the what-if-I-live scenario…

He had a Roth IRA which he hadn’t been able to fund in recent years. He also had 200k of debt. He’s in his young fifties and dedicated to his children, however there comes a time when emphasis needs to shift from the what-if-I-die scenario to the what-if-I-live scenario. Also, one should never fund an annuity (tax-deferred) when eligible but not funding a Roth (tax-free).

We returned the annuity and rejected the new term policy. The dividends on the whole life policy had bought paid up additional insurance which we surrendered for 13k of the 45k cash value. He will use that to fund his Roth for 2013 and 2014. We’ll keep the whole life at least until Roth funding is due for 2015, then maybe whittle it down further or discontinue it altogether if his daughter becomes independent. He’ll apply that extra $1492 to his mortgage.

I explained the rationale behind these decisions to the agent. He acknowledged it made sense, but then added, “I am an insurance salesman”. That code language meant, “My responsibility is to sell policies; besides I’ll forgo a $1k commission if I don’t place the life policy, aside from the $1500 commission I lost not placing the annuity.” I respected his candor and expected him to try to place this term policy. Indeed he did, but my client had a balanced understanding of the risks of both rejecting the policy (premature death) and accepting the policy (opportunity costs) and stood firm.

It’s not a matter of understanding, but of motivation. What saved this client was reaching outside the traditional box of advice exclusively from a salesman, and getting input from someone who understood insurance nuances and the marketplace, investment alternatives, and had the proper motivation. His retirement should be larger, his debt and taxes smaller, while he saves his fee back three times per year for two decades. It started with a phone call.