Comparing Northwestern Mutual’s Term Insurance Case Study # 7

I just finished an insurance review for a Michigan business owner. The results were straightforward and with a company I deal with regularly- Northwestern Mutual. NML is an excellent company, as their agents will tell you, but like all companies they have their strengths and weaknesses. An eclectic strategy can use them for some needs but not all. Even in their strong areas (cash value life insurance) there’s a vast disparity among cash value policies within their portfolio. We addressed that with the Dr. Ryan Wetzel who is featured on our Testimonials page with an accompanying blog.

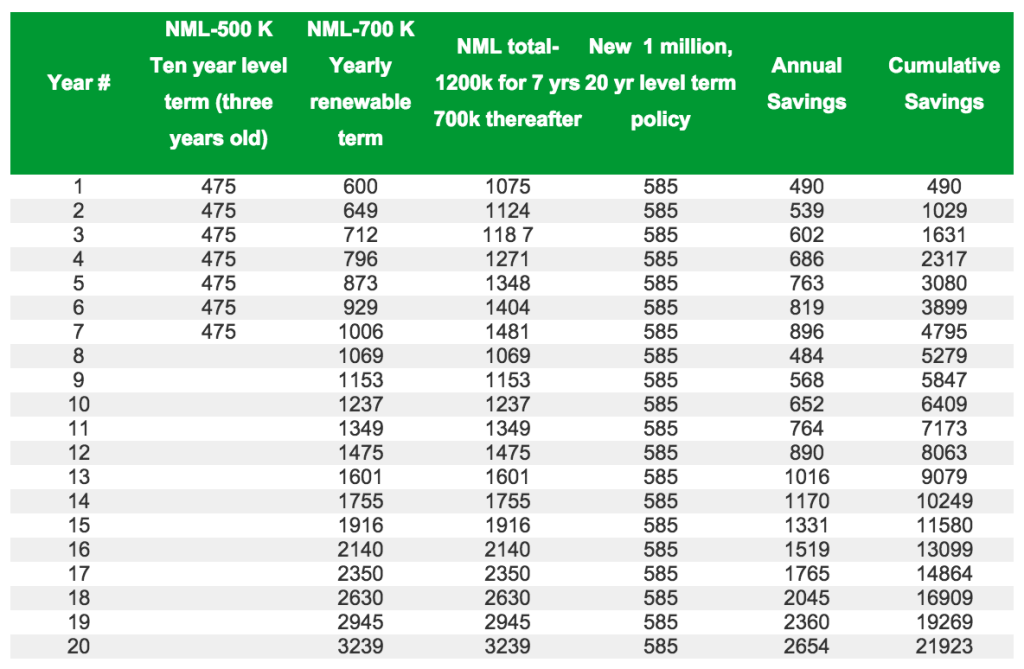

Here I’d like to compare NML’s term life insurance rates to alternatives. The first step is to ascertain the appropriate amount of insurance. This client had $1.2 million of term life insurance with NML. He is well-managed with a strong income, emergency fund, debt-free, and retirement assets. Because of his large young family, should he die, Social Security Survivorship benefits would be over $4,000/month until the children were age 18. This is something he did not fully comprehend. In light of his assets, and after careful review with his wife, they felt comfortable reducing his life insurance to $1 million.

From there it was simply a matter of shopping for a term policy with more favorable rates.

NML’s term insurance was convertible to a more favorable whole life policy, but the client and I discussed this and he was not inclined is to use whole life anyway. The new company’s financial strength was slightly less than NML’s, however this is not as important for term insurance as for cash-value insurance.

He paid me a fee of $675, higher than most reviews. However it took over seven hours of time, carefully and objectively considering his assets, goals, and sentiments. (I also reviewed his Northwestern disability policy which was left intact, and his wife’s life insurance which they changed for additional savings not reflected above.) He adjusted down to a more appropriate amount after having it brought to his attention the survivorship benefits that commissioned agents rarely explain. There were over 50 emails over several months. I walked him through the underwriting process, though I did not sell the replacing term policy.

We got the best of the best; found a strong company with very favorable rates and he got the superlative risk category. It was worth the effort, he will recover his fee the first 14 months and earn (by saving) a substantial tax-free return on his investment, far better than any other way he could “invest” $675.

Most who think they are with a “great” company have little idea of how much they can save. That’s what objective experienced guidance provides and why Scripture so frequently commends it- Proverbs 1:5, 11:14, 15:22, 20:18, 24:6.

Leave a Reply

Want to join the discussion?Feel free to contribute!